Digital Account Application

Designed by Alphie Chen

Directed by Nima H.K.

Type: UX/UI Design

Directed by Nima H.K.

Type: UX/UI Design

Founded in 1985, First Republic Bank was a commercial

bank and provider of wealth management services

headquartered in San Francisco.

“It's a privilege to serve you” is the apropos tagline for

First Republic Bank, as they're known for exceeding

expectations and serving clients in unexpected ways.

The existing First Republic’s digital account application

flow had several problems that resulted in a high drop-off

rate. As a result, the entire flow needed to be redesigned

to address these problems, making it more user-friendly

and easier for clients to open an account online, ultimately

reducing the drop-off rate.

As a product designer at First Republic, my role was

to redesign the digital account application. This page

highlights three major redesigns I worked on: account

type selection, the progress indicator, and address

validation.

Additionally, it showcases the reusable components

we added to the design system for consistency across

other banking products.

bank and provider of wealth management services

headquartered in San Francisco.

“It's a privilege to serve you” is the apropos tagline for

First Republic Bank, as they're known for exceeding

expectations and serving clients in unexpected ways.

Project Overview

The existing First Republic’s digital account application

flow had several problems that resulted in a high drop-off

rate. As a result, the entire flow needed to be redesigned

to address these problems, making it more user-friendly

and easier for clients to open an account online, ultimately

reducing the drop-off rate.

My Role

As a product designer at First Republic, my role was

to redesign the digital account application. This page

highlights three major redesigns I worked on: account

type selection, the progress indicator, and address

validation.

Additionally, it showcases the reusable components

we added to the design system for consistency across

other banking products.

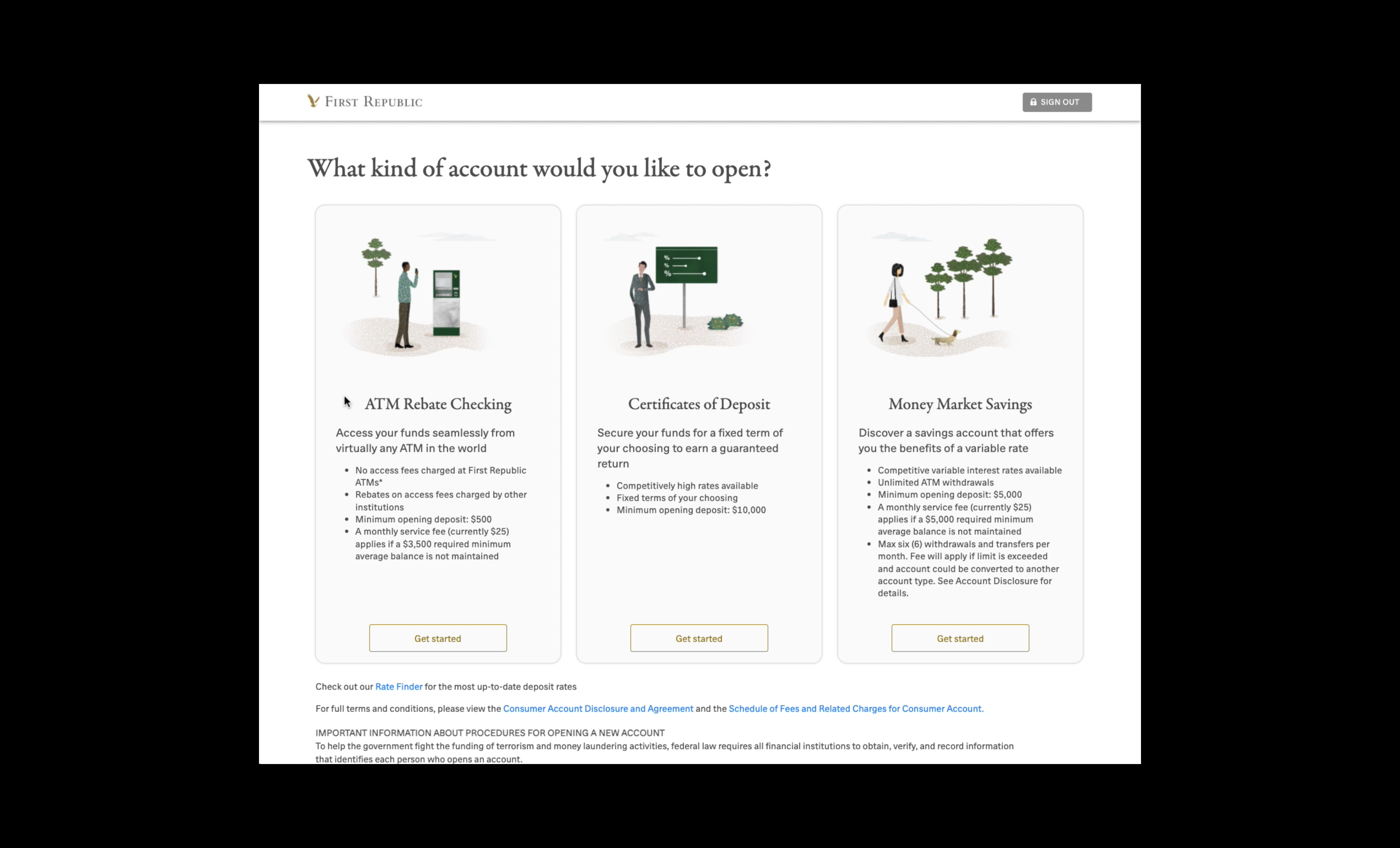

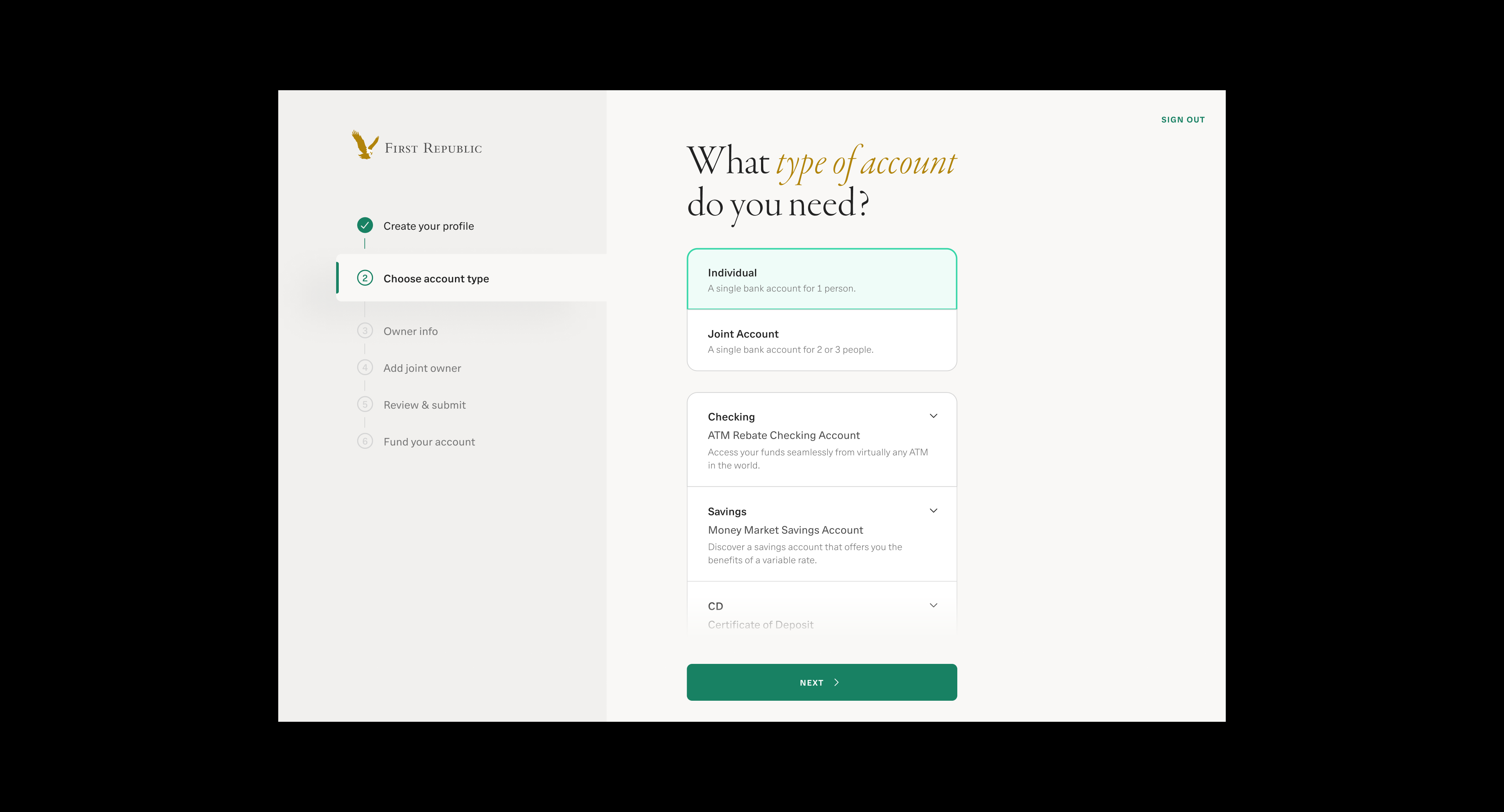

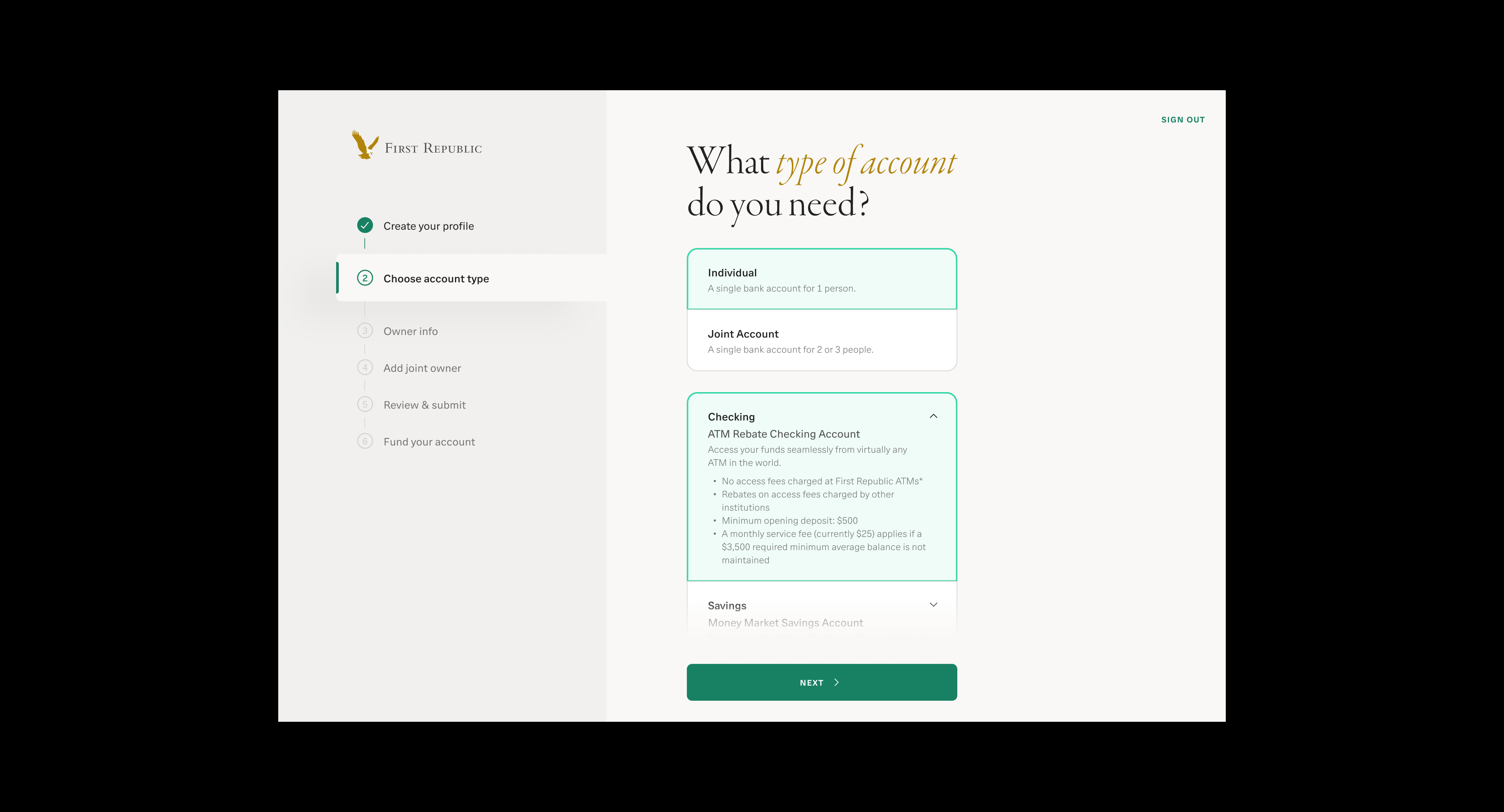

Account Type Selection

Problem

Problem

Data from bankers and the product manager shows a

huge drop-off rate on the Select Account Type page,

caused by confusing account names, poorly organized

information, unhelpful illustrations, and CTA buttons

that are easy to miss.

Goal

1. Simplify Account Selection:

Make account types easy to understand and clearly

indicate from the start that both individual and joint

accounts are available for the three account types:

Checking, Savings, and CD.

2. Organize Information Clearly:

Structure content so applicants can scan and

compare account types quickly.

3. Improve CTA Visibility:

Make the CTA buttons more prominent and easy

to find.

4. Reduce Drop-Off Rate:

Encourage more users to complete the Select

Account Type step successfully.

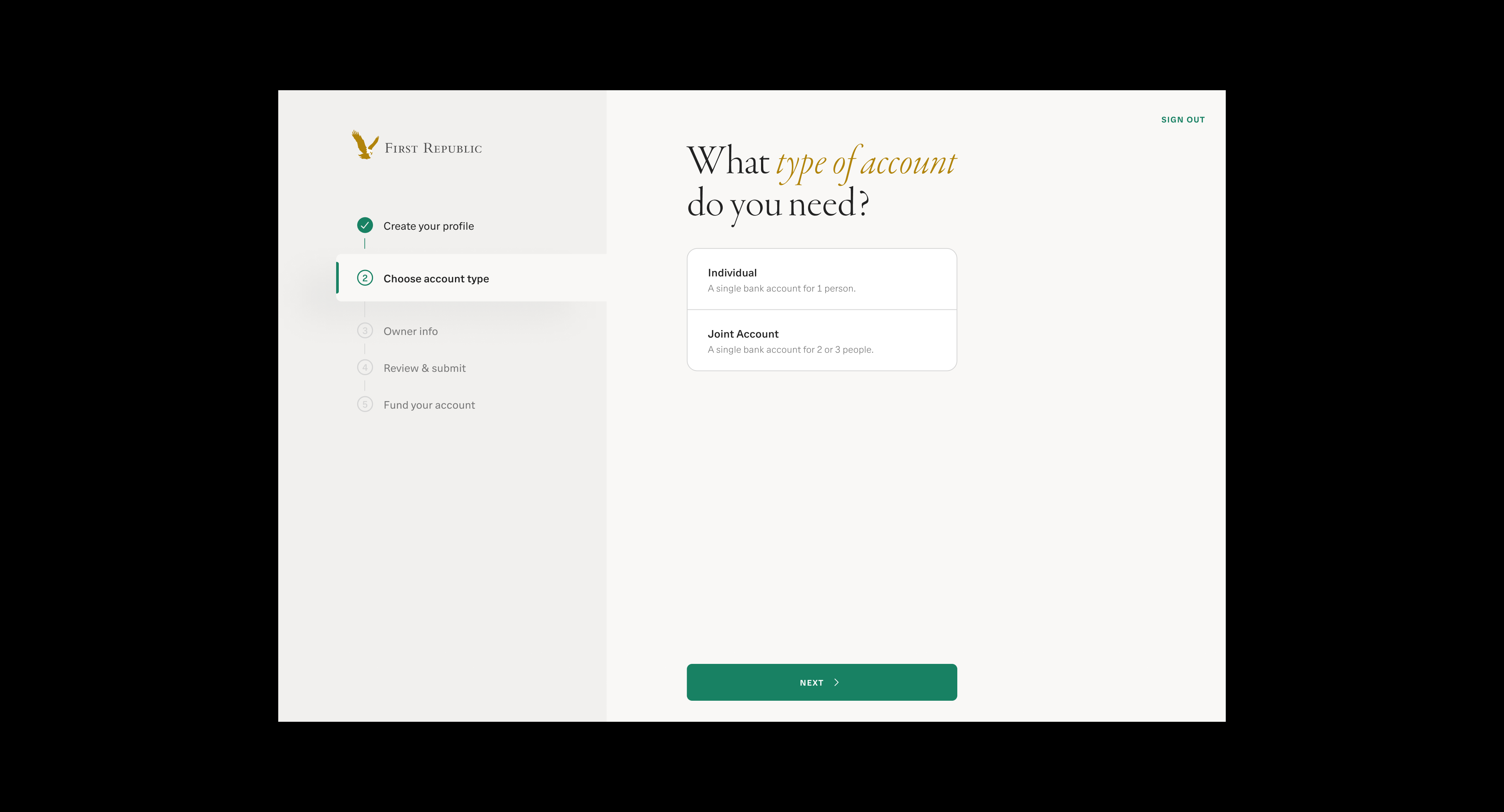

Solution

In the redesign, applicants first choose whether they

want to open an individual or joint account, and then

select the type of account they are interested in.

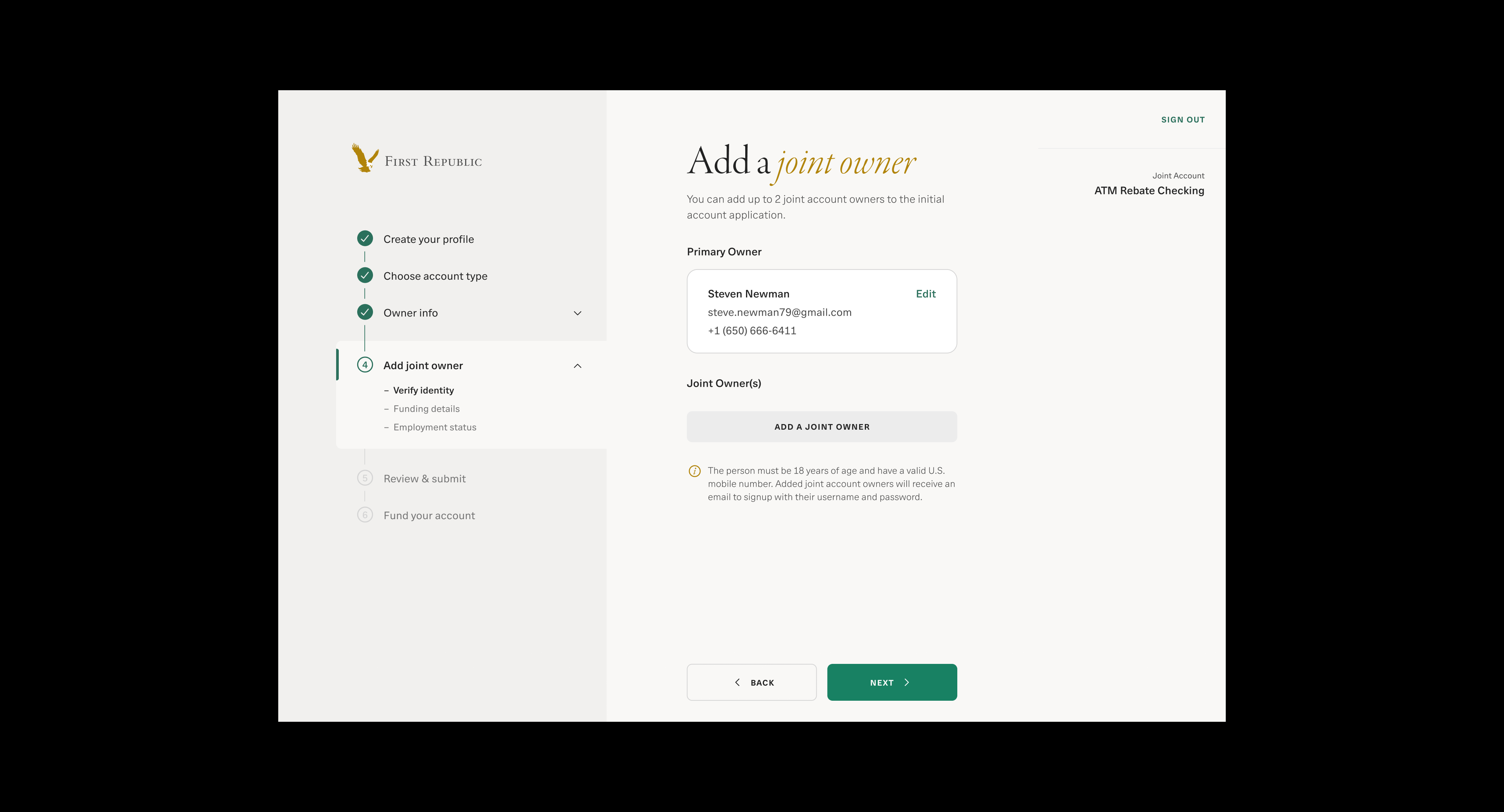

If applicants select an individual account, an additional

step called "Add Joint Owner" will appear in the

progress indicator. This gives them the flexibility

to add one or two joint owners later if they change

their mind. If they choose to skip the joint owner

step, a pop-up will appear to confirm their decision.

If applicants select an individual account, an additional

step called "Add Joint Owner" will appear in the

progress indicator. This gives them the flexibility

to add one or two joint owners later if they change

their mind. If they choose to skip the joint owner

step, a pop-up will appear to confirm their decision.

step called "Add Joint Owner" will appear in the

progress indicator. This gives them the flexibility

to add one or two joint owners later if they change

their mind. If they choose to skip the joint owner

step, a pop-up will appear to confirm their decision.

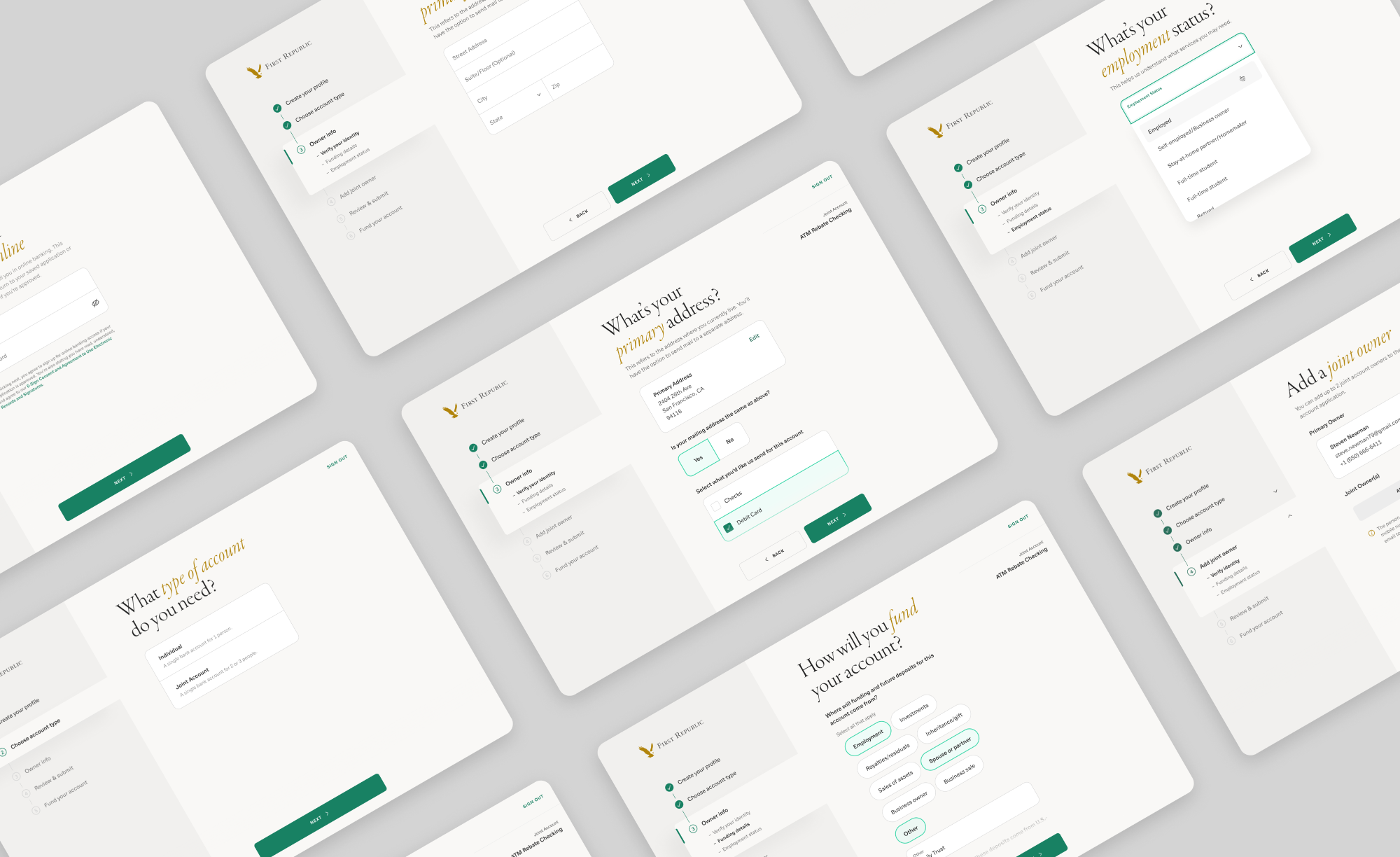

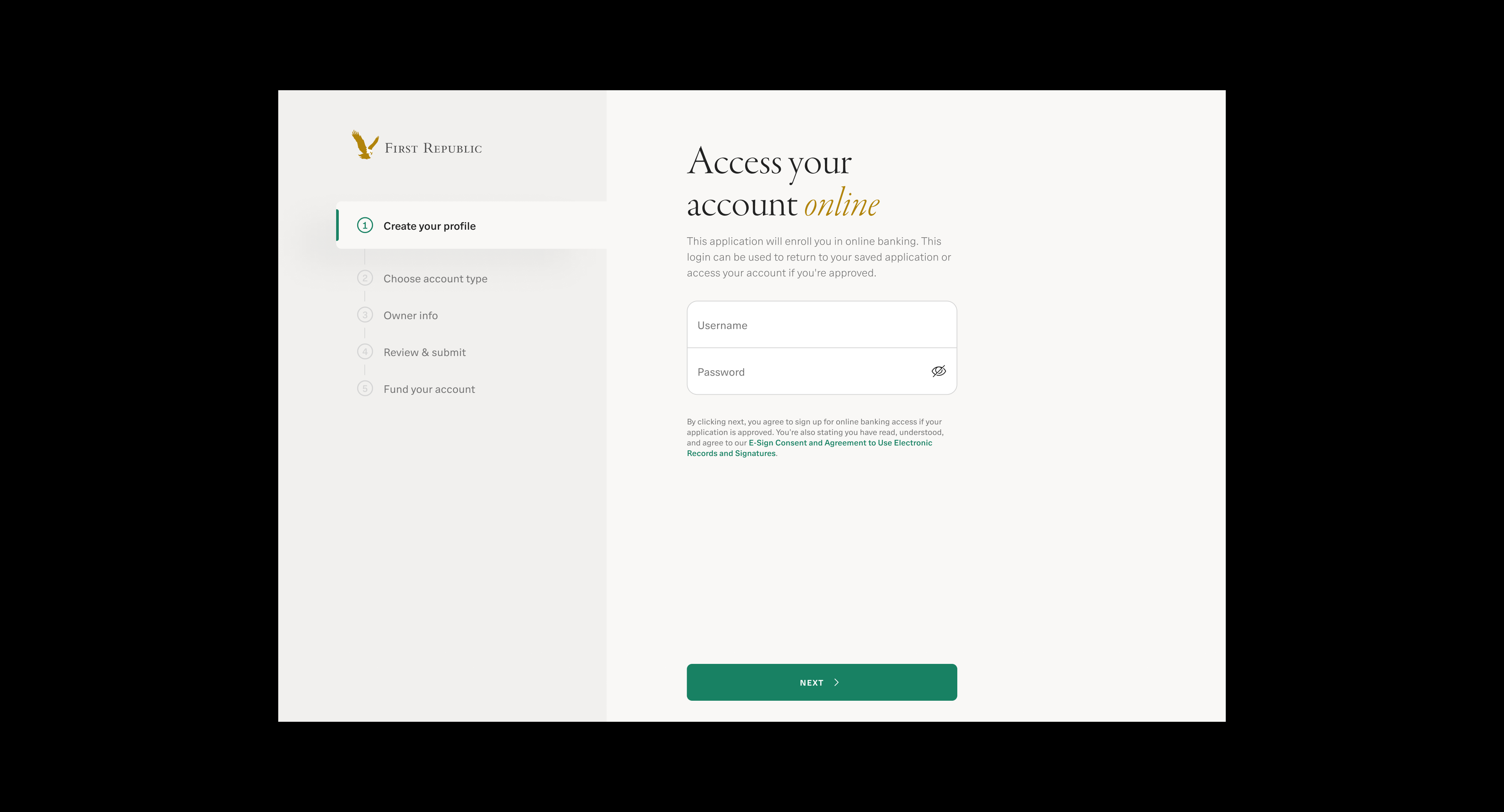

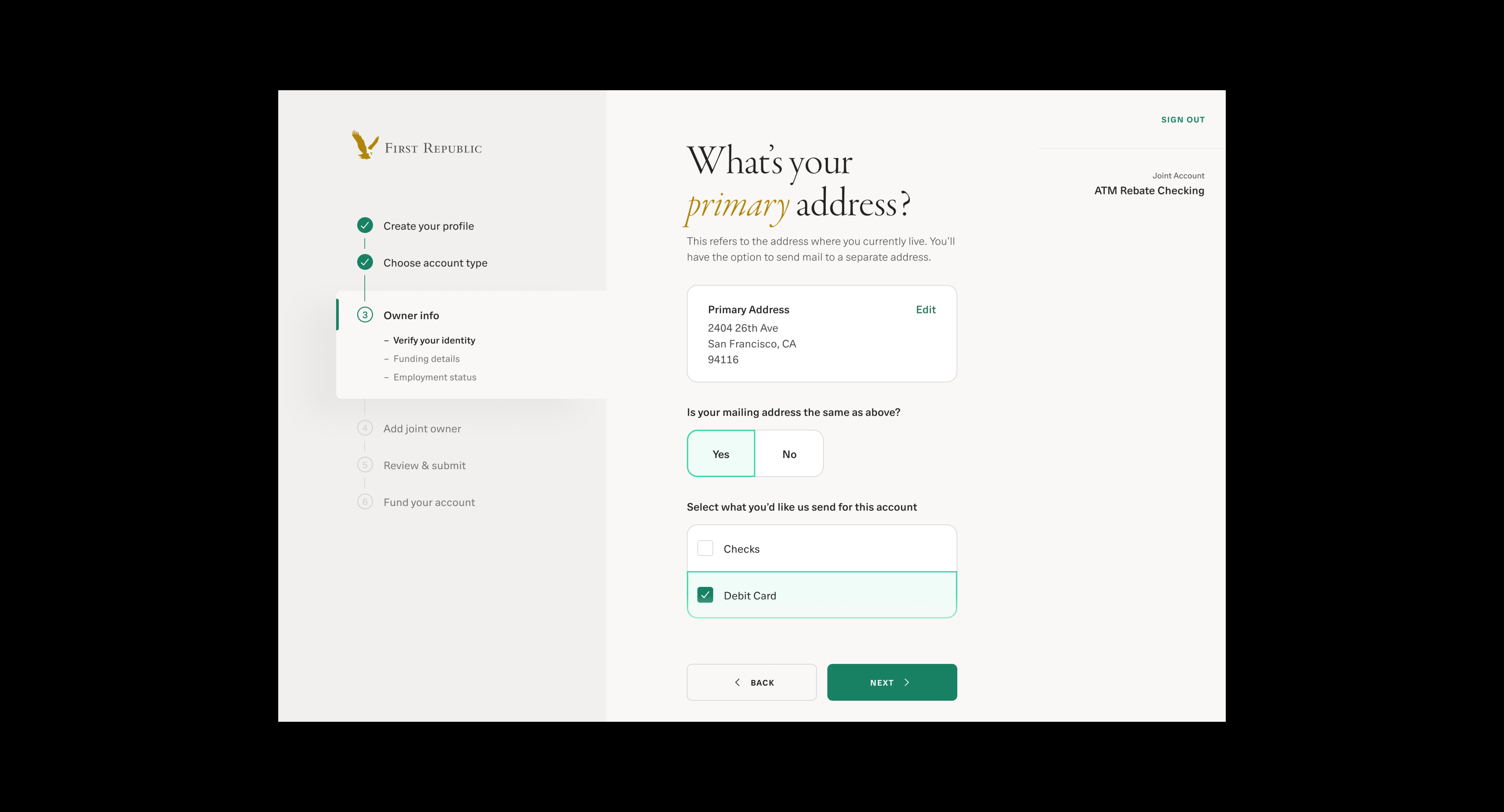

Progress Indicator

Problem

Problem

The existing digital account application flow has a high

drop-off rate due to long-scrolling pages and the absence

of a progress indicator. Without well-structured content

and visibility into their current step and remaining steps,

applicants often become impatient and abandon the

process before completion.

Goal

-

Clear Progress Indication:

Show applicants which step they’re on and how many

steps remain. - Simplify Page Content:

Break up long pages and reduce information overload.

-

Streamline the Flow:

Guide users to move through the application confidently

without feeling lost or overwhelmed. -

Reduce Drop-Off Rate:

Encourage more users to complete the application by

making the process clearer and easier to follow.

-

Clear Progress Indication:

Show applicants which step they’re on and how many

steps remain. - Simplify Page Content:

Break up long pages and reduce information overload.

-

Streamline the Flow:

Guide users to move through the application confidently

without feeling lost or overwhelmed. -

Reduce Drop-Off Rate:

Encourage more users to complete the application by

making the process clearer and easier to follow.

Solution

Introduce a progress indicator and break down the flow

into 6 steps: Create your profile, Choose account type,

Owner info,

Review & submit, and Fund your account.

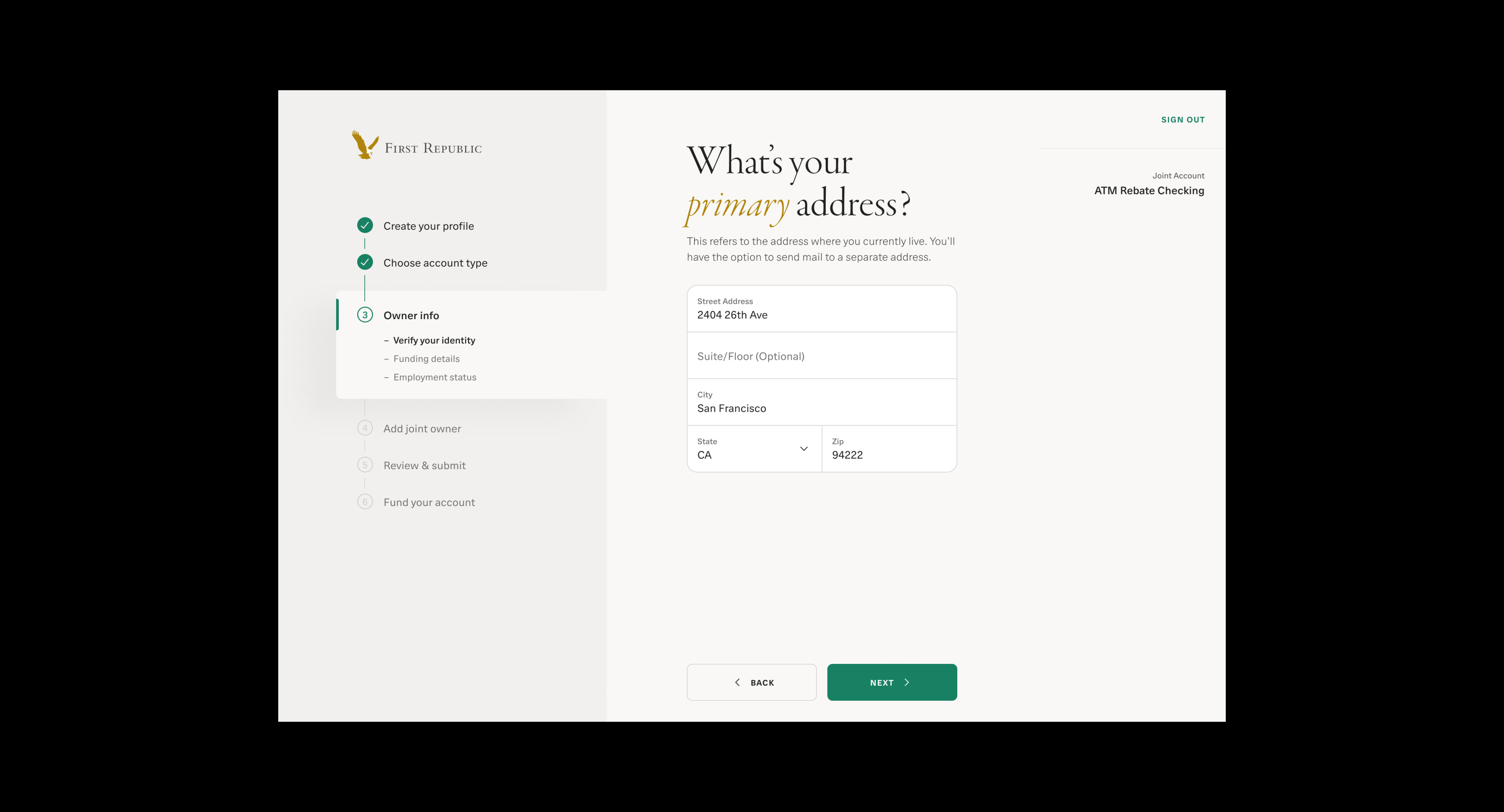

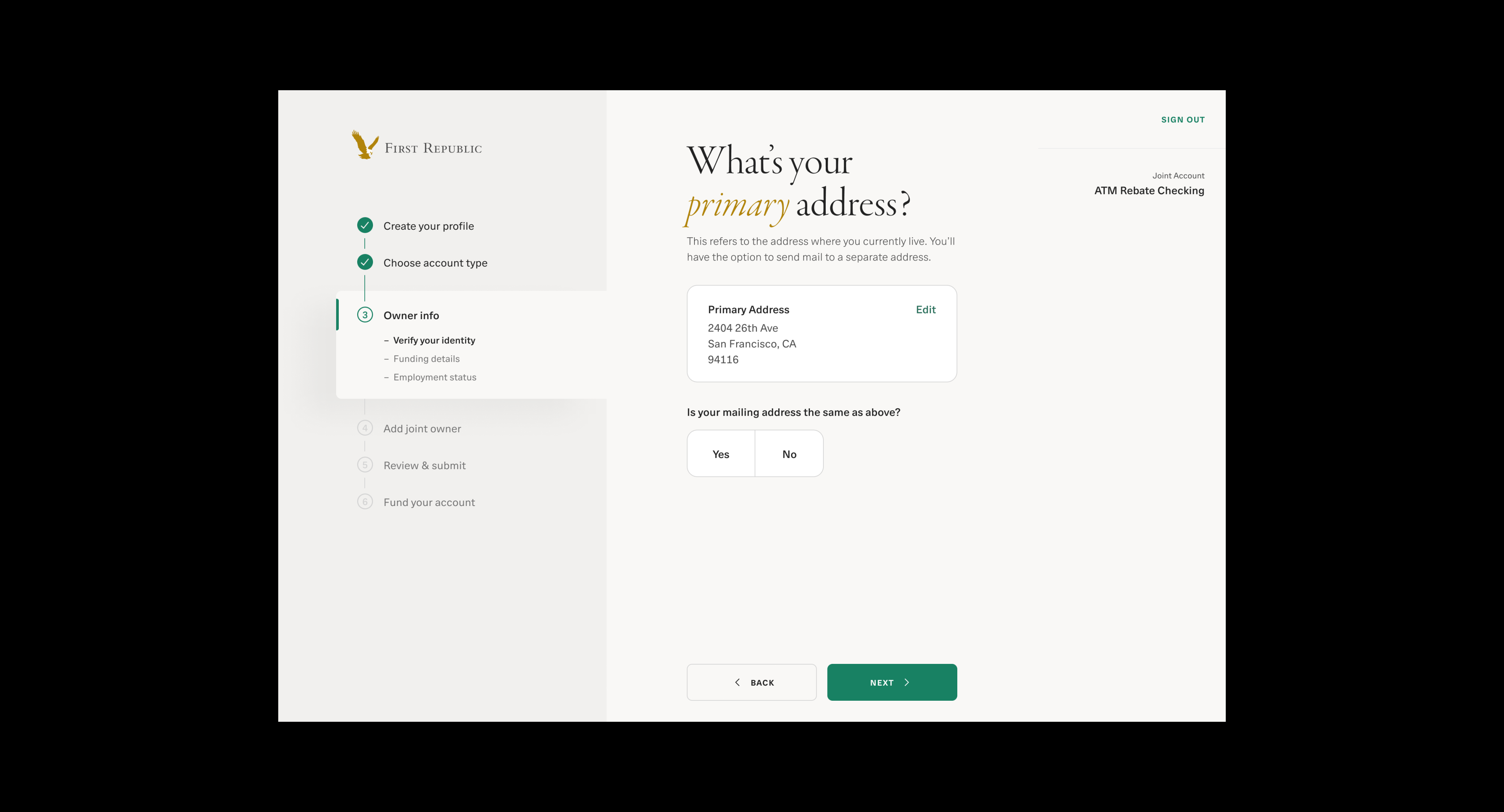

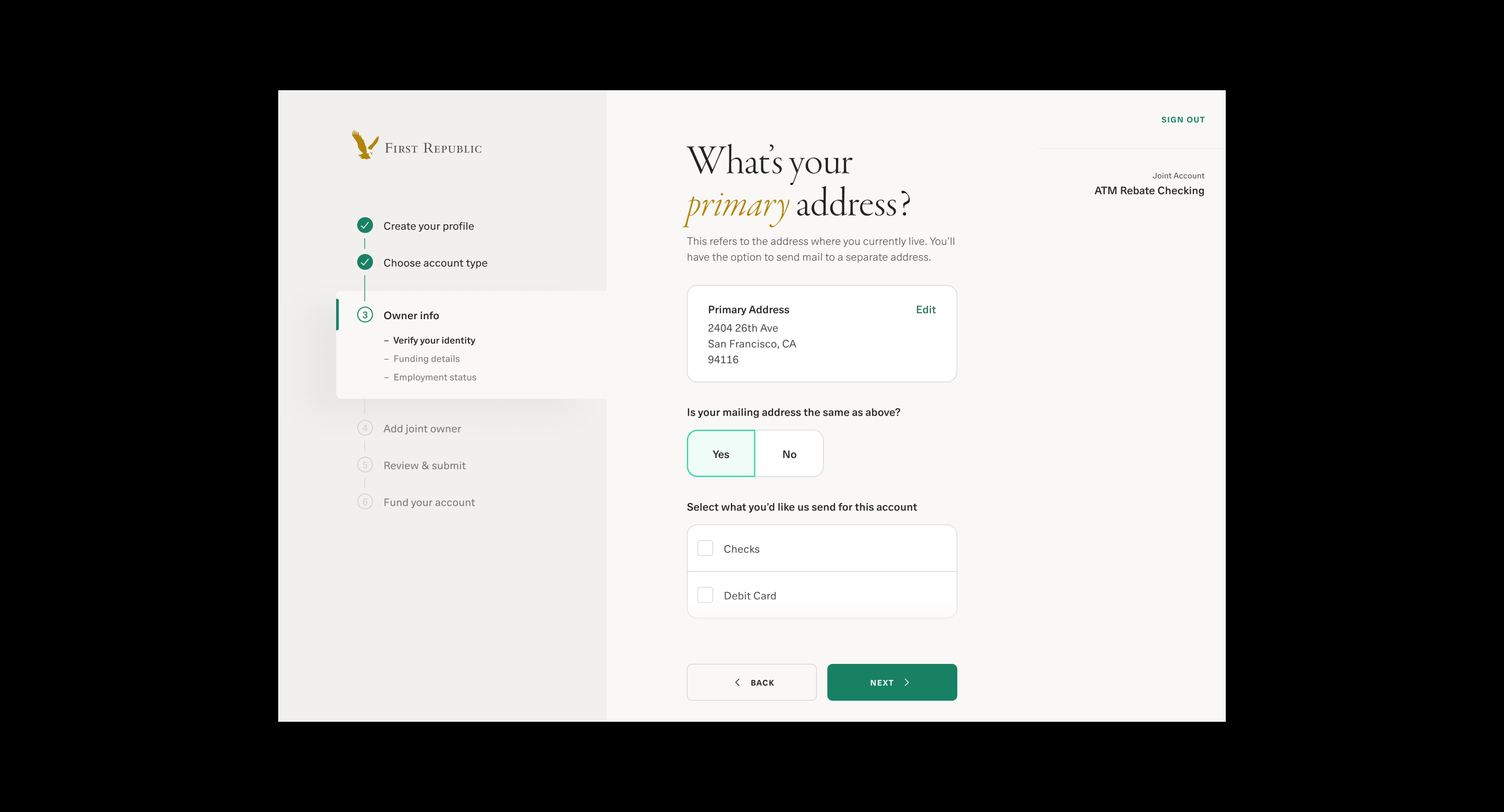

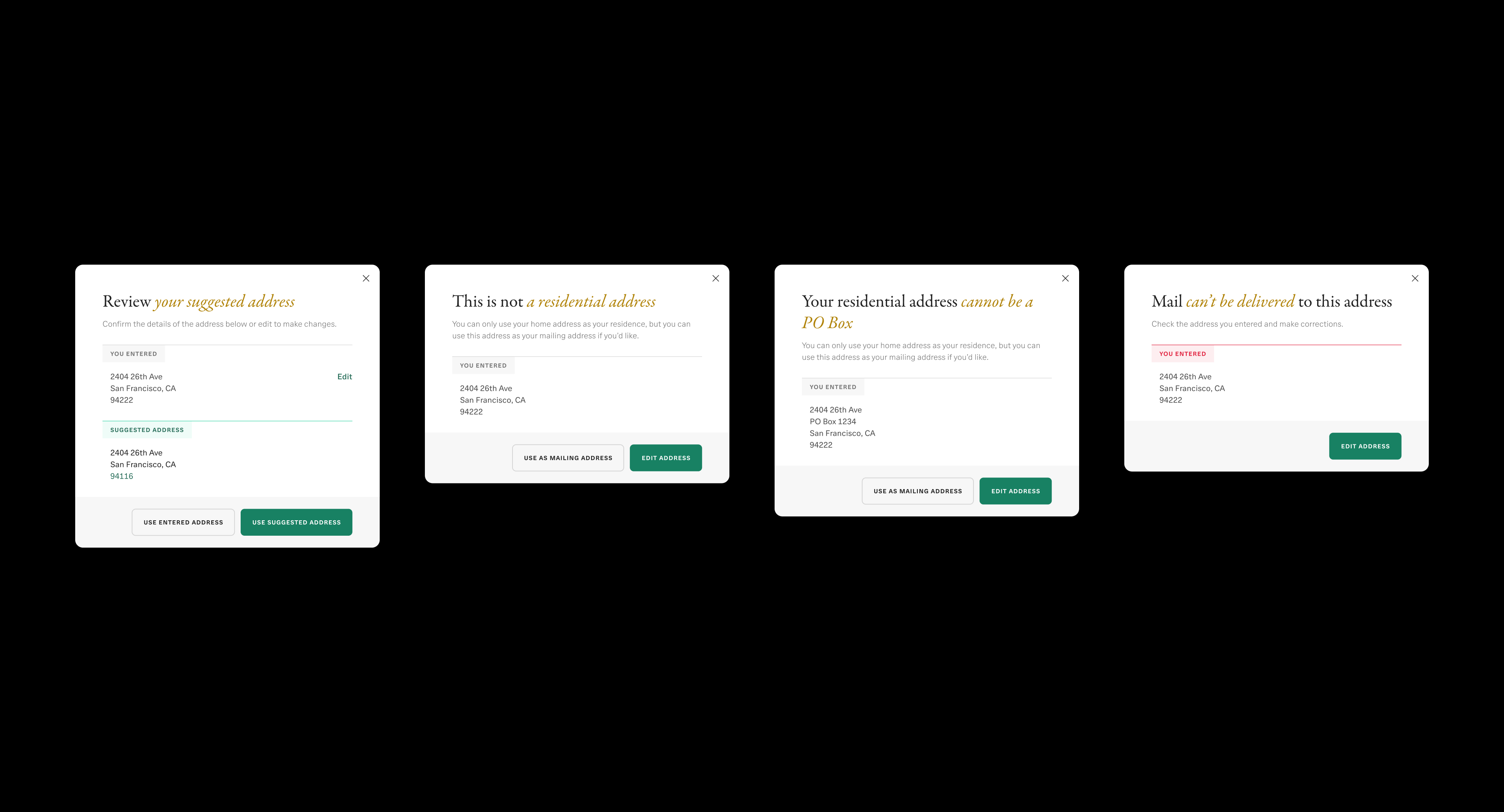

Address Validation

Problem

The lack of address validation and unclear copy led to

invalid addresses for mailing or legal purposes, reduced

address match strength, and negatively impacted risk

scoring for external funding transactions. As a result,

bankers had to reach out to applicants to collect the correct

addresses, which increased back-and-forth communication

and their workload.

Goals

- Ensure Address Accuracy:

Prevent invalid, incomplete, or undeliverable addresses

to comply with bank mailing and legal requirements.

- Improve Risk Scoring:

Increase the probability of accurate matches within the

funding risk model.

- Enhance User Experience:

Provide clear copy and guidance so applicants can

confidently enter their addresses.

- Reduce Banker Workload:

Minimize the need for bankers to contact applicants to

correct address errors.

Prevent invalid, incomplete, or undeliverable addresses

to comply with bank mailing and legal requirements.

Increase the probability of accurate matches within the

funding risk model.

Provide clear copy and guidance so applicants can

confidently enter their addresses.

Minimize the need for bankers to contact applicants to

correct address errors.

Solution

Validate addresses in real time with contextual pop-ups for

5 scenarios to prevent errors and ensure compliance with

bank mailing and legal requirements.

Validate addresses in real time with contextual pop-ups for

5 scenarios to prevent errors and ensure compliance with

bank mailing and legal requirements.

Use Cases

- Happy Path:

If the address is correct, the applicant can proceed

smoothly to the next step. - Suggested Address:

If the address contains a typo or incorrect ZIP code,

a pop-up suggests a USPS validated address. - Non-Residential Address:

If the address is a business address, a pop-up warns that

only a home address can be used as the primary address,

but the applicant can use it as the mailing address. - PO Box Address:

If the address is a PO Box address, a pop-up warns that

only a home address can be used as the primary address,

but the applicant can use it as the mailing address. - Undeliverable Address:

If the address is unknown, a pop-up warns that mail

cannot be delivered.

If the address is correct, the applicant can proceed

smoothly to the next step.

If the address contains a typo or incorrect ZIP code,

a pop-up suggests a USPS validated address.

If the address is a business address, a pop-up warns that

only a home address can be used as the primary address,

but the applicant can use it as the mailing address.

If the address is a PO Box address, a pop-up warns that

only a home address can be used as the primary address,

but the applicant can use it as the mailing address.

If the address is unknown, a pop-up warns that mail

cannot be delivered.

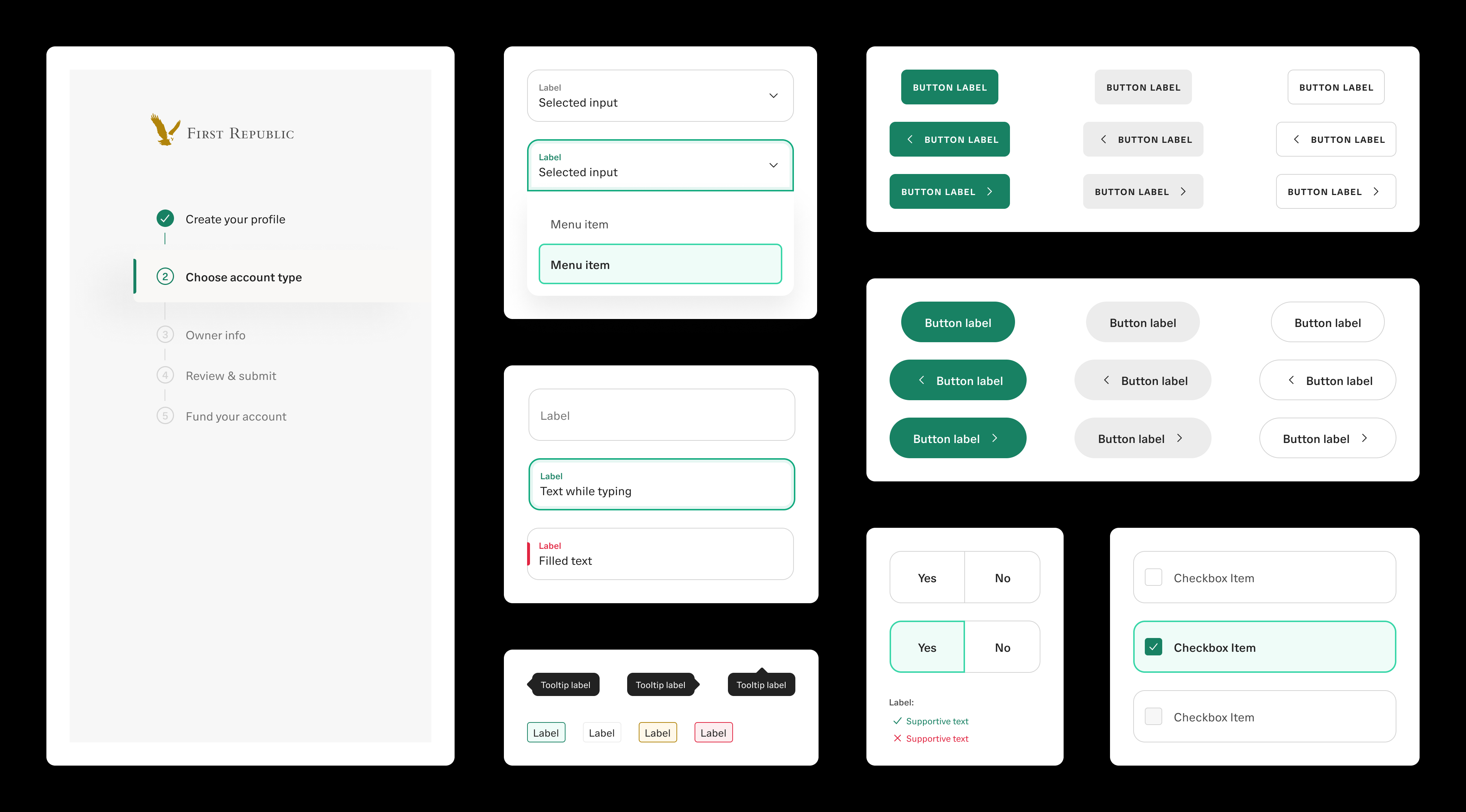

Reusable Components

Beyond redesigning the application, we focused on long-term

scalability by contributing reusable components to the design

system that extend far beyond a single use case.

These components

allow the bank to launch new products faster and more efficiently.

This approach optimized our internal workflow and reduced

development time by 50%.

Beyond redesigning the application, we focused on long-term

scalability by contributing reusable components to the design

system that extend far beyond a single use case. These components

allow the bank to launch new products faster and more efficiently.

This approach optimized our internal workflow and reduced

development time by 50%.

scalability by contributing reusable components to the design

system that extend far beyond a single use case. These components

allow the bank to launch new products faster and more efficiently.

This approach optimized our internal workflow and reduced

development time by 50%.